Policies for Malta's Economic Advancement

We are inspired by the incredible potential of human ingenuity and the entrepreneurial spirit to shape a brighter future for Malta. We believe that the economy can be a powerful force for good, driving positive change for our environment and our society.

It’s time to harness this energy and create a new momentum for Malta, a future where innovation thrives, people flourish, and our island prospers.

To achieve this, we have outlined 17 key measures across four themes: fostering innovation and creativity, investing in our people, streamlining government processes, and ensuring strong and fair enforcement.

A Hub for Innovation and Creativity

Tax Incentives for Innovation

Companies that generate economic activity based on Intellectual Property (IP) will be eligible for a tax incentive. This will apply to all companies that meet the criteria for significant Research, Development, and Innovation (RD&I) investment.

- To qualify, companies must demonstrate a commitment to RD&I by investing at least 10% of their annual turnover in qualifying RD&I expenditures. A proposal for qualifying expenditures is outlined in Appendix 1.

- For the first five years that a company meets the criteria, income generated from IP will be taxed at a 0% rate.

- After the initial five-year period, the tax rate on this income is capped at 10%.

Fostering Beauty in Our Communities

Artists, musicians, and creatives will receive tax incentives to enrich Malta’s cultural landscape.

- Build on the existing 7.5% Tax Rate for Artists by exempting the first €30,000 of income earned.

- Require developers to allocate 2% of large project costs to fund public art installations, murals, or performances in public spaces.

Supporting Sustainable Mobility

Transform the existing car cash allowance into a universal transport allowance by including people who do not own a car and thereby incentivising the use of car-pooling and public transport.

- The existing car cash allowance is available for employees who make use of their own car. This essentially makes €1,170 tax exempt when it is maxed out.

Green Energy Incentives

Incentives for energy security, wind, wave, solar and geothermal.

-

- Incentivising improvements on Energy Use Intensity (EUI) measures and investment in battery storage systems.

- Regional Collaboration for Green Energy with North Africa.

Legislative Innovation

Legislative innovation in the areas of finance through industry working groups focusing on the following sub-sectors: patents, research and artificial intelligence (AI).

-

- Set up expert councils involving representatives of all stakeholders.

- This would operate in a manner similar to that of the Malta Financial Services Advisory Council.

Investing in Our People

Rewarding Integrity

Companies and self-employed individuals who are fully tax compliant (all tax returns are filed accurately and on time while paying any owed taxes in full) will enjoy a reduced tax rate of 25%, encouraging transparency and fairness.

Raise the Bar in Public Procurement

Tax-compliant companies will be rewarded with additional points and preference in tendering processes, while those with a history of underperformance will face penalties.

Fair Wages, Stronger Communities

Introduce a cap on the influx of unskilled third-country workers to create upward pressure on wages, while complementing this with regulatory and market reforms to ensure sustainable wage growth without excessive price inflation. These reforms include reducing bureaucracy, addressing unjustified costs, and improving productivity.

Quotas would be established through detailed analysis of labor market needs, setting specific limits per sector (e.g., construction, hospitality) based on current employment levels, projected demands, and the availability of local workers, with continuous review and adjustment.

Such quotos would be made publicly available internationally so that prospective third-country job seekers would be aware of Malta’s needs.

A Level Playing Field

Businesses that employ a significant percentage of foreign nationals will contribute to local community development.

- Small businesses with less than 50 employees are exempt.

- Businesses employing 30% or more foreign nationals (non-citizens) will pay an infrastructure fee based on a tiered system. The fee increases progressively as the percentage of foreign employees rises.

- The fee is calculated based on the total workforce size and its impact on housing, healthcare, and infrastructure in the local area.

- Fees are higher in areas with greater strain on public resources to ensure fairness.

- Fees will be allocated to local councils as community development funds to support schools, clinics, housing, and public services in the areas most affected.

Bringing Talent Home

Maltese nationals who are currently working abroad and hold level 7 and level 8 qualifications in any field will be offered tax incentives to return and contribute to our growing economy. This scheme will also be available to fresh graduates, thereby incentivising them to stay.

- Returning professionals, who have been abroad for more than 5 years, will be eligible for a flat income tax rate of 15% on earnings for the first 10 years of work in Malta. This is an improvement from the existing scheme which currently only kicks in after 10 years working abroad and lasts only 5 years working locally.

- Fresh graduates will also be eligible for this scheme during the first five years after graduation.

- An individual can only benefit from this scheme once.

Share Option Schemes

Incentivise companies to introduce the means for their employees to buy shares by exclusion from capital gains. This helps promote a fairer distribution of income.

Supporting Affordable Living

Establish a Property Register

The existing 10-year plan for a property register must be expedited.

This would contain information of seller and purchaser price and thereby increasing price transparency with the aim of dampening price inflation in property.

A property register will also prove effective in other areas such as when considering wealth assessment tax.

A Decent Living Wage

A decent living wage is essential to ensuring that workers can afford basic necessities and live with dignity. Our proposal to raise the minimum wage to €360 per week – a €139 weekly increase from the current minimum wage.

- The current minimum wage of €221.78 per week falls significantly short of the cost of living, as highlighted by various studies.

- The most recent Caritas report (2024) estimated a decent living wage at €368 per week, underscoring the growing financial strain on low-income workers. This strikes a balance between economic feasibility and addressing the urgent need for fair compensation.

- This adjustment will help reduce poverty, improve quality of life, and promote a more just and equitable society.

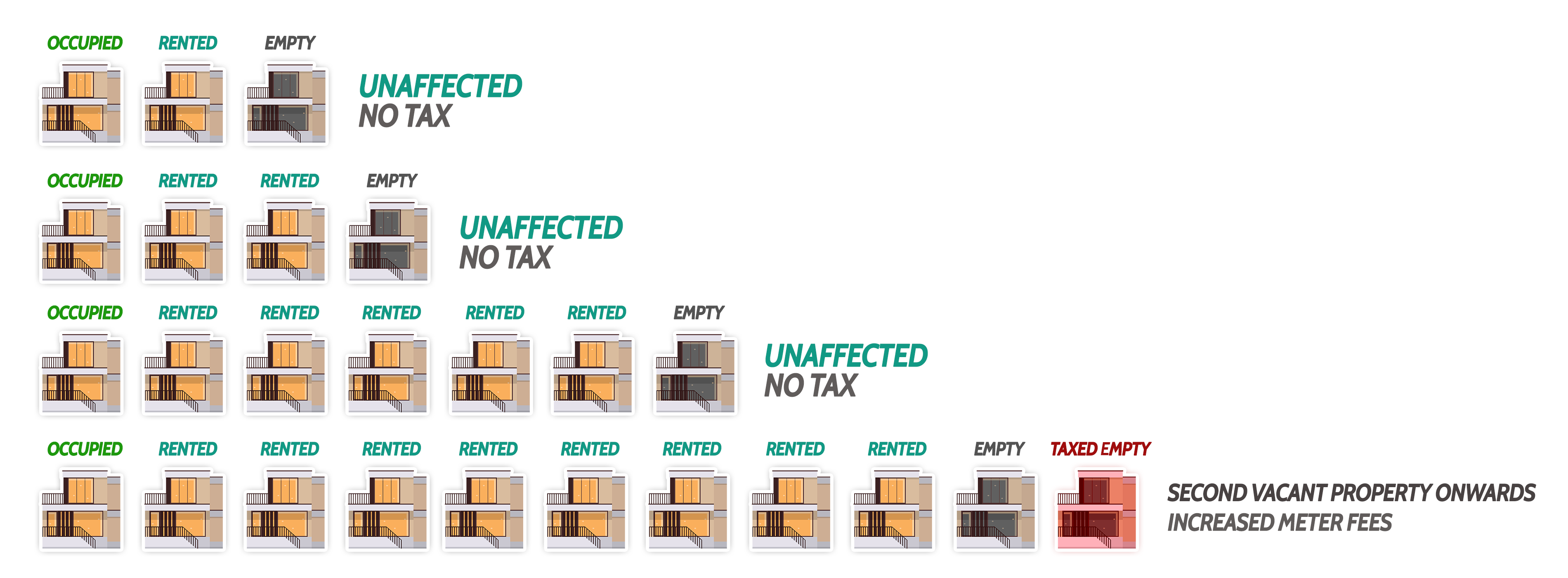

Implement a Tax on Vacant Residential Properties

Excluding the first vacant property. This measure will discourage owners from holding empty properties, lower market prices on purchasing or leasing property, and generate funds for social housing projects.

-

- The Property Register is essential for enforcing this proposal.

- The first vacant property is exempt to protect families with second homes, such as summer residences.

- Applies to vacant residential properties only. Excludes registered rental properties and non-residential properties (e.g., garages, warehouses, offices).

- Vacant properties identified through utility consumption patterns. Exemptions apply to registered rental properties.

- This measure would be implemented through higher water and electricity meter fees on such properties. The number of years a property has been vacant and its size (sqm) are used to calculate multipliers on the standard meter fees.

Streamlining the Public Sector

Smarter Public Services

Conduct a full audit of the public service workforce to identify redundancies and inefficiencies, offering excess workers secondment to the private sector or a voluntary severance package.

Eligibility for severance will be contingent upon a mandatory 5 year exclusion from any future public sector employment, including positions in government agencies, authorities, and entities. This exclusion needs to be rigorously enforced.

Transitioning Talent

Establish an employment office dedicated to supporting public sector employees in transitioning to private sector roles, unlocking their potential in a dynamic economy. Free retraining and re-skilling programmes for such employees.

Full Transparency in Every Government Department and Authority

Significantly increase the resources of the National Audit Office (NAO). Require the compulsory submission to the NAO of all transactional data from all departments and authorities with a maximum of a 3-month delay. This must take the form of an accessible and structured digital format (see FAIR principles) and should also be published by the NAO for external bodies to be able to apply further scrutiny.

- Invoices with description and value

- Payments

- Suppliers

- Employees on payroll

- Role

- Grade

- Hours worked

- Name and ID Card

- Salary will not be published

Appendix 1 – Qualifying RD&I expenses

Personnel Costs:

- Salaries, wages, and bonuses paid to employees directly involved in RD&I activities. This includes researchers, scientists, engineers, technicians, programmers, and support staff dedicated to RD&I projects.

- Employer contributions to social security, health insurance, pension plans, and other employee benefits for RD&I staff.

- Training costs specifically related to enhancing the skills and knowledge of RD&I personnel in areas relevant to their research activities.

Direct Costs of RD&I Activities:

- Cost of raw materials, components, and supplies consumed or used in RD&I experiments, prototypes, or pilot projects.

- Cost of lab equipment and software used exclusively for RD&I, including purchase, lease, maintenance, and repair. Depreciation of such assets can also be included.

- Payments to external contractors or consultants for specialised RD&I services, such as data analysis, testing, or prototype development.

- Costs associated with obtaining and maintaining patents, trademarks, and copyrights related to the results of RD&I activities.

- Costs of developing and testing prototypes and pilot models..

Payments to Research Institutions:

- Grants, contributions, or fees paid to universities, research institutes, or other non-profit organisations for conducting collaborative research projects.

- Payments for accessing specialised research facilities or equipment at universities or other institutions.

Exclusions:

- Selling and distribution costs.

- General administrative and management expenses not directly related to RD&I.

- Costs of routine software maintenance and bug fixes (as opposed to developing new features).

- Costs of acquiring existing technology or intellectual property, as opposed to developing new IP (unless the acquisition is a prerequisite to being able to develop the IP further).

- Construction or renovation of buildings (unless dedicated solely to RD&I).